Robo Advisor vs. Online Broker for Dummies (Like Me)

ROBO ADVISOR vs. ONLINE BROKER

A Gen X Guide to Rocking Your Retirement Investments

WAIT! Before you scroll past this post thinking it is just another snooze-fest about finance, hear me out. This might be one of the smartest moves you make for your future. Seriously.

For many of Gen X, terms like “investment portfolio,” “asset allocation,” and “tax optimization” sound intimidating. They seem like they belong in the boardrooms of Wall Street or the scripts of financial thrillers. But here is the truth: thanks to tech, investing is not just for the rich and famous anymore. It is for anyone with a smartphone. All you need is a few bucks. You also need a desire to make your money work harder than your 9-to-5 ever did.

Here, we break it down—no jargon, no judgment. This is a clear, honest look at two powerful tools. They can help you build wealth and plan for retirement: robo-advisors and online brokers. We compare them across five key categories. Also, we explore who they are best for. Finally, we help you decide which one deserves a spot in your financial band.

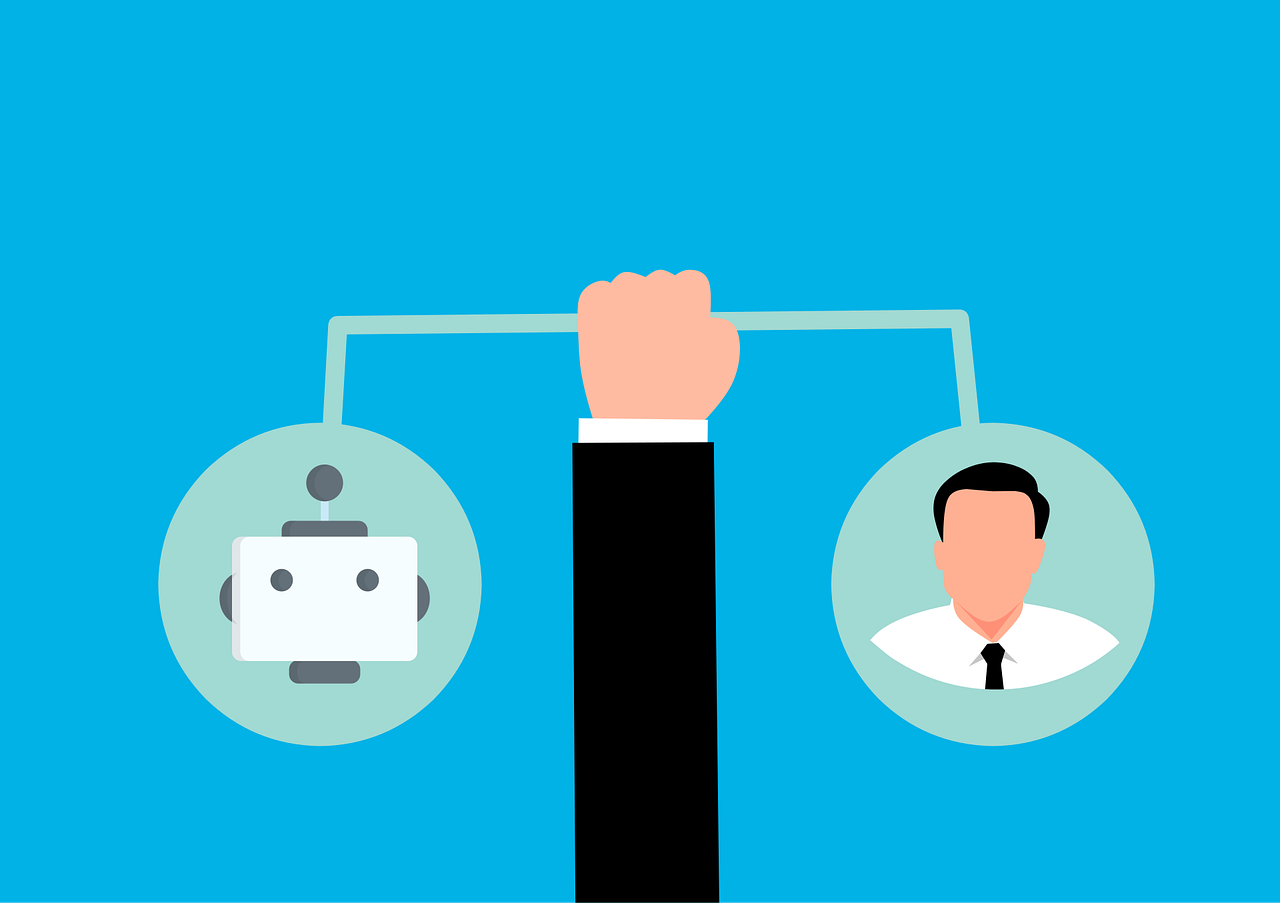

What Are These Tools Anyway?

Robo-Advisors

Think of robo-advisors as your automated roadie—they handle the behind-the-scenes setup so you can focus on the show. These platforms use algorithms to manage your investments based on your goals, risk tolerance, and timeline. They are efficient, low-cost, and perfect for hands-off investors. Examples include Acorns, Betterment, and RocketMoney.

Online Brokers

Online brokers are the human advisors you meet through platforms like Zoom or phone calls. They offer investment guidance, yes—but also help with retirement planning, estate strategies, and tax navigation. They are like your financial producer, helping you craft a custom strategy based on your unique situation. Think Charles Schwab, Merrill Lynch, or independent advisors.

The Breakdown: Robo vs. Broker

| CATEGORY | ROBO ADVISOR | ONLINE BROKER |

| Cost | Lower fees | Higher fees |

| No minimum investment | Account minimums | |

| Affordable for small portfolios | Comprehensive services justify cost | |

| Investment strategy | Passive approach | Customizable |

| Driven by algorithm | Active management | |

| Automatic Rebalancing | Behavior guidance | |

| Personalization | Standardized advice | Highly personalized |

| Limited human interaction | Relationship oriented | |

| Convenience | Available 24/7 | Availability depends on advisor |

| User friendly platforms | Highly specialized | |

| Investments only | Broad range of services | |

| Expertise/Trust | Algorithm reliability | Experienced judgement |

| No human emotion | Trust/Accountability | |

| Best for | Beginner investors/simple needs | Those with complex portfolios |

| Tech-savvy individuals | Those who value personal help | |

| Those seeking low costs | Those with significant wealth | |

| Passive, hands-off investors | Those seeking active management | |

Who is Best Suited for Each?

Robo-Advisors Rock For:

- Beginner investors with simple goals

- Tech-savvy folks who love automation

- Budget-conscious users who want low fees

- Passive investors who prefer “set it and forget it”

Online Brokers Rock For:

- People with complex financial lives (businesses, real estate, etc.)

- Those who want personalized, face-to-face advice

- Investors with significant wealth or legacy planning needs

- Anyone who values emotional support during market swings

Can Robo-Advisors Handle Retirement Planning?

Absolutely. Robo-advisors are not just for dipping your toes into investing—they can help you build a solid retirement strategy. Most support Traditional IRAs, Roth IRAs, and SEP IRAs. They will guide you through setting long-term goals, choosing tax-advantaged accounts, and adjusting your asset allocation as you age.

Some even use “glide path” strategies, which gradually shift your investments from aggressive to conservative as you approach retirement. It is like having a financial GPS that reroutes automatically as your destination gets closer.

If you want to automate your savings, robo-advisors are a fantastic option. They help you avoid micromanaging your portfolio. They are the ultimate backstage crew—quietly keeping everything running while you focus on living your best encore life.

But What About the Human Touch?

Here is where online brokers shine. Robo-advisors are great for efficiency. However, they cannot match the depth of service and emotional intelligence that human advisors bring to the table.

A good financial advisor does not just manage your money—they help you manage your mindset. A good financial advisor is there when markets dip. They are present when panic sets in. They also assist when you are navigating a career pivot. Whether selling a business or planning a legacy, they are there to guide you. They ask questions, listen deeply, and help you make decisions that align with your values.

Yes, they cost more. But for many, that cost is worth the peace of mind and strategic insight they provide. It is like hiring a producer who knows your sound and your audience. They understand your goals. They help you craft a financial album that hits all the right notes.

So Which One Should You Choose?

Here is the truth: there is no one-size-fits-all answer. Your choice depends on your financial goals, your comfort with technology, and how much control you want over your investments.

If you are just starting out, robo-advisors are a great way to get in the game. They help keep costs low. You should choose them if you prefer a hands-off approach. They are efficient, reliable, and perfect for building momentum.

If you are juggling multiple income streams, you might consider an online broker. If you are planning for retirement with nuance, they can also be the better fit. Or, if you simply want someone to talk to about your financial future, they may be a great choice. They will help you navigate complexity with clarity and confidence.

And guess what? You do not have to choose just one. Many investors use a hybrid approach—automating basic investments with a robo-advisor while consulting a human advisor for big-picture planning. It is like having both a killer playlist and a live band.

Final Take: You are the Headliner

Whether you go digital or personal, the most important thing is that you start. Investing is not reserved for the elite. It is a tool for anyone who wants to build wealth. You can gain freedom. You can also rock your retirement on your own terms.

So do not let fear or confusion hold you back. Explore your options. Ask questions. And choose the financial strategy that fits your rhythm.

Because when it comes to your future, you are not just a spectator—you are the headliner. And it is time to take the stage.

As an Amazon Associate, I earn from qualifying purchases. These links help keep the lights on and the mixtapes rolling—thank you for supporting Retirement Rockstars.